Table of Content

Discover How to Develop an App Like Affirm for BNPL Business Success

The “Buy Now, Pay Later” (BNPL) sector has experienced explosive growth in recent years, revolutionizing how consumers make purchases, particularly online. Apps like Affirm have spearheaded this movement, offering a flexible and transparent alternative to traditional credit.

By allowing users to split the purchase costs into manageable installments, BNPL services have gained popularity among a wide demographic, attracting both the tech-savvy and budget-conscious shoppers. The appeal lies in the convenience, often interest-free options, and the ability to acquire goods and services immediately while spreading out the payments over time. This burgeoning market presents a significant opportunity for entrepreneurs and developers looking to create innovative financial technology solutions.

Developing a successful BNPL app like Affirm requires a deep understanding of the underlying business model, the technical complexities, and the regulatory landscape governing financial transactions. In this comprehensive guide, we will explore the steps involved in developing a BNPL app similar to Affirm in 2025. We will explore the core concepts behind BNPL, and discuss the roadmap for the development process used by professional mobile app development services.

Let’s begin.

What is Affirm? A Comprehensive Overview

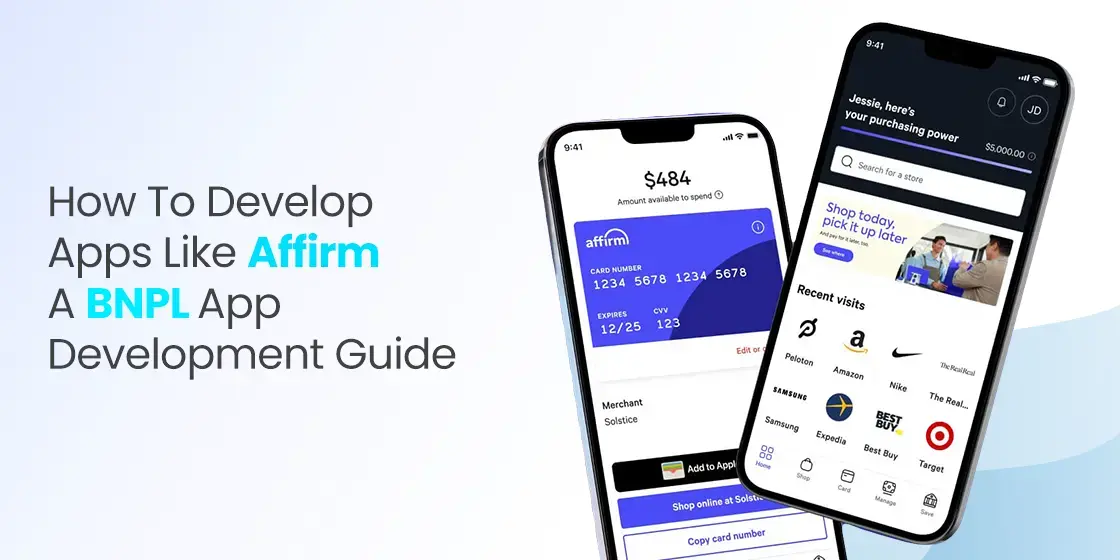

Affirm is a leading financial technology company that provides “Buy Now, Pay Later” services to consumers. Founded in 2012, Affirm has established itself as a prominent player in the BNPL market, partnering with a vast network of online and in-store retailers across various industries, including fashion, electronics, home goods, and travel.

The core offering of Affirm is to allow shoppers to divide the cost of their purchases into fixed monthly installments, often with transparent terms and no hidden fees. Unlike traditional credit cards, Affirm provides consumers with a clear repayment schedule and the total amount of interest they will pay (if any) before they complete their purchase.

These plans can range from a few months to several years, depending on the purchase amount and the retailer’s offerings. Affirm clearly displays the monthly payment amount and the total cost of the purchase, including any applicable interest. Once the customer agrees to the terms, the purchase is completed, and Affirm manages the subsequent repayments directly with the consumer.

How Does Affirm Stand Apart from Its Competition?

Affirm differentiates itself from some other BNPL providers, such as apps like Dave, through its emphasis on transparency and responsible lending practices. The company often offers interest-free options for smaller purchases or through partnerships with specific retailers. For larger purchases where interest applies, Affirm clearly discloses the Annual Percentage Rate (APR) and the total interest payable upfront. Moreover, it is now emphasizing no-interest loans on its platform too.

This commitment to transparency and its focus on providing consumers with clear and predictable payment terms have contributed significantly to Affirm’s widespread adoption among both consumers and merchants. The company’s success has highlighted the growing demand for flexible and transparent payment alternatives in the modern retail landscape.

Understanding the “Buy Now, Pay Later” Business Concept

The “Buy Now, Pay Later” (BNPL) business concept represents a significant shift in consumer financing, offering an alternative to traditional credit cards and installment loans. At its core, BNPL allows consumers to make purchases immediately and pay for them in smaller, scheduled installments over a defined period.

This model has gained traction due to its convenience, often lower (or zero) interest rates compared to credit cards for shorter repayment periods, and its seamless integration into the online and increasingly in-store checkout processes. The appeal is particularly strong among younger demographics who may be wary of traditional credit or are looking for more flexible payment options.

The BNPL business model typically involves a tripartite relationship between the consumer, the merchant, and the BNPL provider (like Affirm). When a consumer chooses to pay with BNPL at a participating merchant, the BNPL provider pays the merchant the full purchase amount upfront (minus a transaction fee).

The consumer then enters into a repayment agreement with the BNPL provider, making scheduled payments over the agreed-upon term. The revenue streams for BNPL providers generally come from two primary sources: transaction fees charged to the merchants for each BNPL purchase facilitated on their platform, and interest charged to consumers for longer-term repayment plans or larger purchase amounts.

How to Develop Apps Like Affirm in 2025 – A Detailed Guide

Knowing how to develop apps like Affirm in 2025 requires a well-structured approach encompassing several key stages. Let’s take a look at each individual step of the finance app development process in greater detail.

Define Your Requirements and Core Features

The initial phase of development involves clearly defining the scope and functionality of your BNPL app. Conduct thorough market research to identify unmet needs and potential differentiators. Determine your target audience, the types of purchases you will support (e.g., online only, in-store, specific product categories), and the repayment options you will offer (e.g., number of installments, interest rates, fee structure).

Define the core features your app will include, such as user registration, credit assessment, purchase initiation, repayment scheduling, notifications and reminders, and customer support features. Consider any unique features you want to offer to stand out from existing BNPL apps, such as personalized offers, loyalty programs, or integration with budgeting tools. A well-defined set of requirements will serve as the foundation for the entire development process.

Design and Set Up the App Architecture

A robust and scalable app architecture is crucial for a financial application that will handle sensitive data and potentially high transaction volumes. Choose a suitable technology stack for your front-end (user interface) and back-end (server-side logic and database).

Consider factors like performance, scalability, security, and development team expertise when making these decisions. Plan for the integration of third-party services, such as payment gateways, credit bureaus, and identity verification providers. Consider using microservices architecture for better scalability and resilience.

Develop the App Frontend (UI/UX)

The user interface (UI) and user experience (UX) are critical for a BNPL app, as they directly impact user adoption and satisfaction. Design an intuitive and user-friendly interface that makes it easy for users to register, apply for financing, manage their purchases and repayments, and access customer support.

Focus on a seamless checkout experience within merchant integrations. Ensure the app is visually appealing, responsive across different devices (mobile and web), and adheres to accessibility guidelines. Conduct thorough user testing to gather feedback and iterate on the design to optimize usability and engagement.

Develop the App Backend and Third-Party Integrations

The backend of your BNPL app will handle the core logic, data management, and integrations with external services. Develop secure and efficient APIs for user authentication, credit assessment, transaction processing, repayment management, and notifications. Integrate with payment gateways to facilitate fund transfers between the BNPL provider, merchants, and consumers.

Connect with credit bureaus and identity verification services to perform real-time credit checks and ensure user identity. Implement robust error handling and logging mechanisms for monitoring and troubleshooting. Ensure your backend infrastructure is scalable and reliable to handle a growing user base and transaction volume.

Set Up and Audit Security Protocols for Financial Transactions

Security is essential for any financial application, and BNPL apps are no exception. Implement end-to-end encryption for all sensitive data, both in transit and at rest. Follow industry best practices for secure coding and regularly audit your codebase for vulnerabilities. Implement strong authentication and authorization mechanisms to protect user accounts and prevent unauthorized access.

Comply with relevant financial industry standards and regulations, such as PCI DSS if you are handling cardholder data. Implement fraud detection and prevention measures to identify and mitigate suspicious activity. Regularly conduct security testing and penetration testing to identify and address potential weaknesses in your system.

Test and Deploy

Thorough testing is crucial before deploying your BNPL app to ensure its functionality, security, and performance. Conduct various types of testing, including unit testing, integration testing, user acceptance testing (UAT), and security testing. Address any bugs or vulnerabilities identified during the testing phases.

Plan your deployment strategy carefully, considering factors like scalability, reliability, and rollback mechanisms. Monitor the app closely after deployment to identify and resolve any issues that may arise in a live environment. Regular updates and maintenance will be necessary to address bugs, introduce new features, and adapt to evolving market needs and regulatory requirements.

Essential Features All Apps Like Affirm Should Have

To be competitive in the BNPL market, your app should include a range of essential features common to all of the top fintech mobile apps in the Middle East, or Europe, US, or more. They include:

- User Registration and Profile Management: A seamless and secure process for users to create and manage their profiles, including personal information, payment methods, and linked bank accounts.

- Credit Assessment and Approval: A fast and reliable system for real-time credit checks using integrations with credit bureaus and proprietary risk assessment algorithms. Clear communication of approval status and available financing options.

- Purchase Initiation and Management: An intuitive interface for users to select BNPL as a payment option at participating merchants, view available installment plans, and agree to the terms. Clear display of payment amounts, due dates, and any applicable interest or fees.

- Repayment Scheduling and Management: A clear and easy-to-understand repayment schedule with options for automatic payments, manual payments, and viewing payment history. Notifications and reminders for upcoming payments to minimize defaults.

- Merchant Directory and Integration: A comprehensive list of partnered merchants where users can utilize the BNPL service. Seamless integration with merchant checkout processes via APIs and SDKs.

- Notifications and Alerts: Timely notifications regarding payment schedules, upcoming due dates, successful payments, and any account-related updates.

- Customer Support: Multiple channels for users to seek assistance, such as in-app chat, FAQs, email support, and potentially phone support. Efficient handling of inquiries and issue resolution.

- Security Features: Robust security measures, including data encryption, secure authentication, fraud detection, and compliance with relevant financial and data privacy regulations.

- Transaction History: A clear and detailed record of all past and pending BNPL transactions, including purchase details, repayment schedules, and payment status.

- Optional Features: Consider adding features like personalized offers based on user behavior, loyalty programs, the ability to refinance purchases, or integration with personal finance management tools to enhance user value.

FAQs

| How can you create a payment app? In order to build a payment app, you need to: Analyze your requirements Plan the project milestones Design the UI/UX Develop the backend Coordinate with the regulatory bodies Test and deploy |

| What is the best alternative to Affirm? Sezzle is said to be the best alternative to the Affirm app. |

| Is Affirm a loan app or a BNPL app? Affirm offers both BNPL services as well as loans to its consumers. |

Conclusion

Knowing how to develop apps like Affirm in 2025 presents a significant opportunity within the rapidly evolving fintech landscape. However, it requires a comprehensive understanding of the BNPL business model, careful planning, robust technical execution, and an unwavering commitment to security and regulatory compliance.

By following a detailed development guide, entrepreneurs and developers can create innovative BNPL solutions that cater to the growing demand for flexible and transparent payment options. The key to standing out in this competitive market lies in identifying unmet needs and offering unique value that resonate with both consumers and merchants.

Empower your digital journey with StruqtIO - Your dedicated partner for cutting-edge custom software development, innovation, and digital transformative solutions. Harness the power of technology to elevate your business and redefine your digital landscape today.